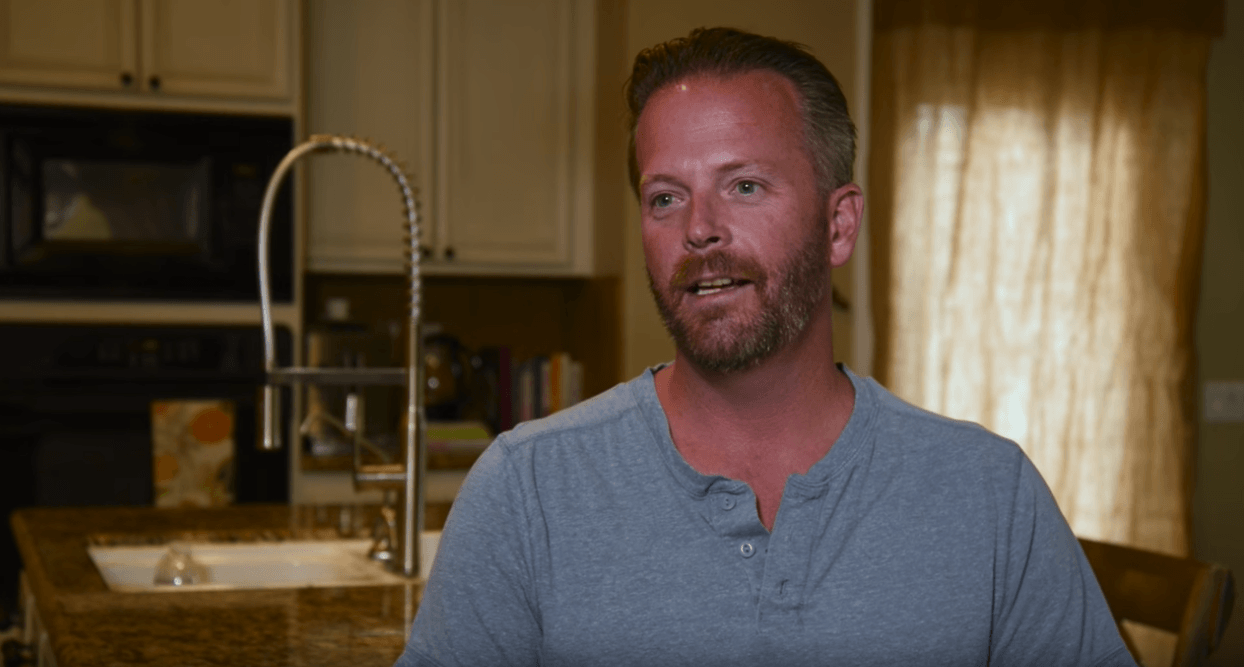

See how one homeowner used an Equity Sharing Agreement to pay off $45,000 in credit card debt without adding new monthly interest or payments.

If you’ve checked your savings account lately and wondered, “Is this rate actually good?”, you’re not alone. At any given time, the answer depends on three things.

In the second part of our series, we’ll walk you through how to fund, purchase, and make the most of your second property investment, while maintaining flexibility and minimizing risk.

Looking to make your home smarter? Discover practical smart home upgrades that save time, add convenience, and increase value – without the frustration or high costs of unnecessary gadgets.

For many homeowners, the idea of buying a second property represents more than just a second real estate purchase. It’s a vision of financial freedom, flexibility, and future security – whether that means having a vacation spot to enjoy, a rental home generating income, or a nest egg that can grow in value over time.

Mortgage rates are still high in 2026. Learn why homeowners are skipping cash-out refinancing & what equity alternatives make more sense in today’s market.

Learn how much to budget for home repairs and renovations over the lifetime of a home. See annual and monthly averages, regional differences, and smart ways to plan.

Unison helped this homeowner pay off debt and remodel their home with home equity funds.

It's easy to focus on the list price of a home, while ignoring the amount of interest that will likely accrue over the lifespan of your mortgage. Here's how to manage it and stay prepared.

PMI adds an additional monthly payment to your budget, but you may be able to avoid it completely. Read on for the easiest ways to reduce or remove the need for PMI entirely.

Cash-Out Refinancing is more popular than ever. The process of getting approved tends to be faster than a HELOC, but how long does it actually take?

Due dates get missed – it's just part of life! But it's important not to make a habit of missing these deadlines, especially on payments as significant as your mortgage.

While a 20% down payment is typically the gold standard, it may not always be financially feasible. Read on to weigh up the pros and cons of 10% and 20% down mortgages.

.jpg)