See how one homeowner used an Equity Sharing Agreement to pay off $45,000 in credit card debt without adding new monthly interest or payments.

Housing is a huge market, but it's difficult for investors to put their money in homes without owning them outright. Learn more about how co-investments help bridge the gap.

A HELOC may be an affordable and convenient way to access a line of credit. But it’s not the right solution for everyone. We'll explain how a HELOC works and how to know if it’s right for you.

The "Zestimate" is a bit of a secret sauce, which Zillow will admit is not always perfect. But it's a valuable tool nonetheless – here's what we know about the calculation process.

If you're planning on putting less than 20% down, you'll likely need to anticipate paying for PMI. But how much of a burden is it? Read this article for some of the common amounts to expect.

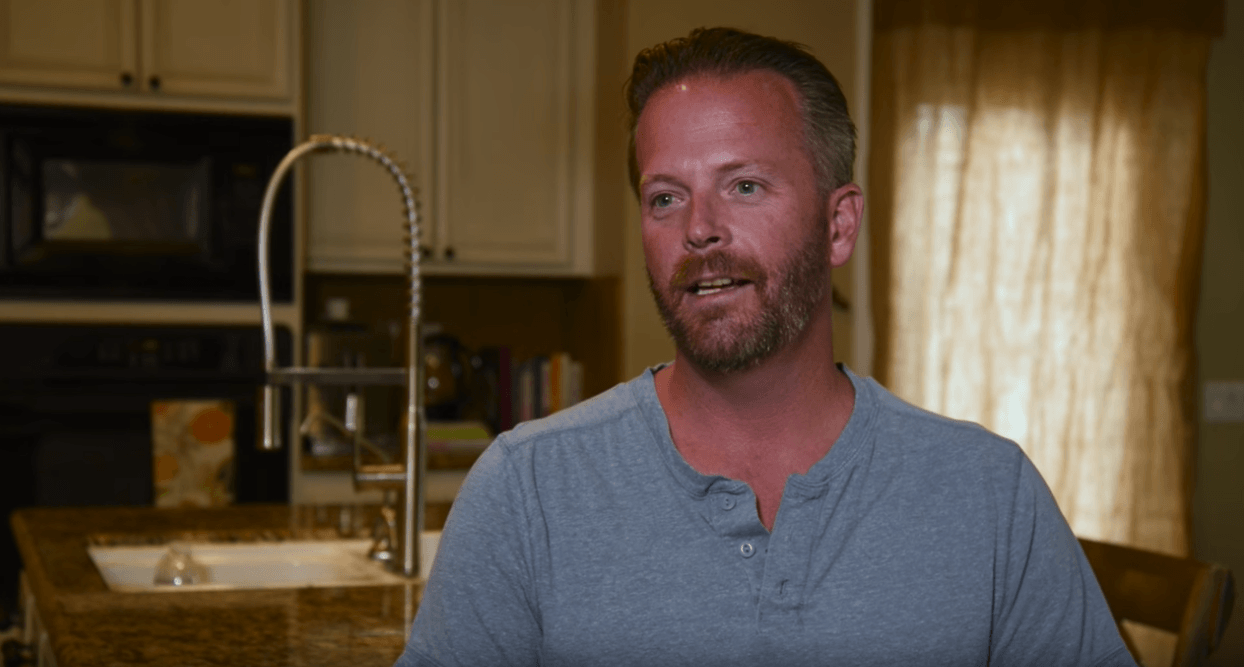

Leslie and John weren't sure about their next move – between debt, renovations, and bills. With a home equity sharing agreement from Unison, they didn't have to choose.

Unison helped this homeowner pay off debt and remodel their home with home equity funds.

Learn how you can keep the value from your home improvements. We explain the Remodeling Adjustment in our Equity Sharing Agreement.

Learn how we share in the ups and downs of your home's value. Discover how an Equity Sharing Agreement works when it is time to sell or finish your term.

Learn how Unison determines your home’s value through OAV and EAV. Our guide covers appraisals, risk adjustments, and closing fees for equity sharing.

Learn how a Equity Sharing Agreement can help you access home value without monthly payments or interest. Discover a new way to fund your life goals.

If you’ve built up meaningful equity in your home and could use some extra flexibility, you’ve probably come across something called a Home Equity Investment (HEI).

High-interest debt is squeezing homeowners in 2026. Learn how to consolidate debt using home equity—without refinancing or adding another monthly payment.

.jpg)

.png)